Engineering economics, which I studied in college, and have put into practice on hundreds of projects in my career, is the comparison of the TOTAL LIFETIME costs (or net cash flows) of a set of project options to determine which has the lowest cost, or will save the most money for the business.

{Note: I have to give credit to my kids - they’re very bright and encouraged me to write this all out!}

A complete analysis would include the upfront purchase cost of all materials, construction labor, ongoing maintenance, overhauls and replacement parts, consumables (like fuel), taxes, insurance, legal/regulatory costs, and more. On the other side of the equation would be the various benefits – revenues, risk reduction, service improvement, maybe salvage value – some of which are intangible, but generally are considered as part of a business decision to engage in a project. Then all the costs and benefits (cash flows) for each year of the project life are brought back to today’s dollars via the Net Present Value (NPV) calculation, and an “equal dollars” comparison can be made.

In some cases, we might want to look at the projects evaluated to a common future value of cash and assets. This is uncommon in project engineering economic analysis, but rather frequently looked at by individuals planning for future needs – such as retirement funds.

Why should I care about all this?

So, if you told you that you could put an extra $750K into your retirement by changing just one daily activity, would you do it? Would you even believe it possible?

No, not your latte. No, you don’t have to do anything uncomfortable.

We all gotta eat. And we know food isn’t cheap. (And the cost keeps getting higher, which is part of the value of this exercise / habit change, as we’ll see.)

So we’ve all made those PB&Js for the kids to take to school. You’ve probably heard your kids say, “Why can we BUY lunch? There’s a restaurant across the street and EVERYBODY goes there.” No way. Well did they get that example from us parents? How many times do you go out for lunch at work? Maybe we should set an example and practice what we preach? Well, there is a really good reason to do just that.

Say let’s make some assumptions about what we spend going out during work, and about what the “brown bag” option costs. Then we’ll do the math and watch magic happen!

Brown bag:

My typical bag lunch might consist of: a peanut butter and jelly sandwich ($0.70), some crackers or chips ($0.20), some cookies ($0.15), (in a few baggies $0.06) and an apple ($0.45), with water. Total cost, $1.56.

Restaurant:

You could look at anything from fast food like McDonalds on up to full table service, say Applebee’s. I’m going to assume $10 on average. And remember about 50 cents for gas, depending on distance. So $10.50 each time.

Calculate:

Every day you bring instead of buying, you save $8.94. I assume 43 weeks a year (because of holiday, vacation, and days that either lunch is provided, or you get stuck buying. Times 5 days a week and the savings is $1922.10 in the first year.

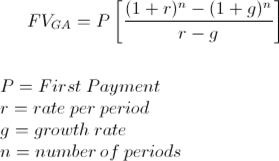

Now food costs keep going up, so the savings will increase each year. Therefore we will be using the formula for the “future value of a growing annuity”, which is:

The inputs are:

P = $1922.10 (the first year savings)

r = .08 (8% annual returns on investment, based on the average annual return of the S&P 500 stock index over the last 40 years*)

g = .03 (3% growth in the annual savings)

N = 40 (40 years of saving, based on a career lasting from age 22 to age 62 - so this is better for someone just starting out.)

Build the formula in Excel, and it figures to $739,103. About three-fourths of a MILLION $$$ !

You may already have this habit. Congratulations! And you probably know it’s saving you money. But did you realize the amount? That’s the power of steady investing and compounding over a long period of time. And that’s what we want to do more of.

FOOTNOTE:

* You’re investing for the long term, so you put it in equities - an S&P 500 index mutual fund. From January 1, 1979 to December 20, 2018 (a period just weeks short of the 40 years we are using in this analysis), the S&P had an average annual return of 8.35%. So we’ll use 8% here to make it simpler.